The Nonpartisan Leader Newspaper, February 10, 1919, Page 4

You have reached the hourly page view limit. Unlock higher limit to our entire archive!

Subscribers enjoy higher page view limit, downloads, and exclusive features.

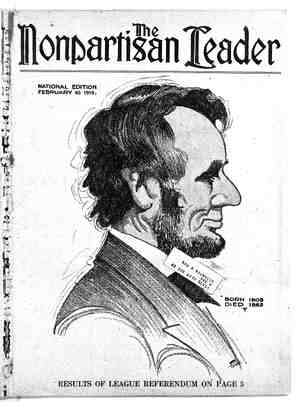

N. D. State Bank Has Man Fundamental Part of Legislation for the People Modeled on Federal Reserve BY WALTER W. LIGGETT OST important of all the bills pending before the North Da- kota legislature is that creat- ing the Bank of North Dakota. It is the cornerstone of the which the League farmers in- tend to rear in that state—and most of them frankly admit the structure can not be built without this firm financial foundation. With the Bank of North Dakota in oper- ation;: however, it is certain that the state- owned terminal elevator and flour mill system will succeed, that the state’s vast lignite de- posits may be developed, that the home-saving bill can be inaugurated, and that, backed by its own public funds, the state can finance its own institutions if outside bankers refuse be- cause of political prejudice. Finance is the basis of all business and the Nonpartisan league legislative experts displayed great wis- dom when they refused to embark upon their program of state-owned industries until they had provided a method of sound banking. There is nothing experimental about the pro- posed Bank of North Dakota. Neither is it any way “revolutionary.” It simply is a carefully con- sidered measure which combines the best features of the Federal Reserve bank and the farm-loan act and adds to this several constructive features pat- terned after the Australian land banks and the co- operative farm loan associations of Europe. Both the Federal Reserve bank and the farm loan act now meet with a very general ap- proval—although both were bitterly opposed by bankers prior to their passage—and the Bank of North Dakota is designed to do for that state what these other two measures have done for the na- tion as a whole. MEETS APPROVAL OF SOME BANKERS Already the proposed measure has been approv- ed by many North Dakota bankers and one of the leading financiers of the state has privately ad- mitted that while it injures his personal interests —which really are involved with a Minneapolis institution—it will be a boon for the independent bankers of the state and ‘benefit business as a whole as well as promote agricultural production. Certainly, this is exactly the effect the Bank of . North Dakota will have if the experience of other eommonwealths - is any criterion as to the result of similar legislation in North Dakota. South Australia has had a state land bank in operation for 26 years and in 1911, out of a - population of 411,464 people, there were 179,- 478 depositors. In other words, 44 per cent of the entire population-of South Australia had deposits in the state bank and these deposits averaged nearly $200 each, or mearly $80 per capita. No state in the United States can boast such a record. It also is a fact that a larger pro- portion of workingmen own their own homes in South Australia than anywhere else in the world. i West Australia also-has a land bank and in 1914, after it had been in operation for 21 years, it -had the wonderful record of never having evicted a borrower or foreclosed a mortgage, and, although it loaned approximately $8,000,000, it never lost a penny in bad debts and was operated at a profit. The managing director of the South Australian land bank declared its operation was so suec- cessful' that the other Australian states were forced to enact similar legislation to keep their populations from migrat- ing to South Australia. Australia is- not the _ sentatives. splendid new industrial edifice - only place where land banks have proved success- ful.. They are in operation in Russia, Germany, Italy, New Zealand, Switzerland, practically all the British colonies, Sweden, Denmark and Holland. Ireland is another example of what a land bank does to promote prosperity. Forty years ago Ire- land was the most impoverished of all the British After studying their state bank plan, no one can have any doubts as to the seriousness of the farmers’ reform ef- forts. It is the crucial test, for finan- cial power is the backbone of all spe- cial privilege. No. milk and water re- formers would thus break the back of the interests opposed to the people. It distinguishes the Nonpartisan league from so many of the reform move- ments we have had in recent years, which attempt to solve the problem of plutocratic rule by slapping the fat boys on the wrists and calling them very hard names. The platform which is going through in North Dakota is also another proof of the integrity of the League leaders. The enemies of- the League in fact can not point to a -single instance where the League has failed -in its promise to the farmers. -All has gone through as scheduled. Farmers were organized, campaigns put on and the fight for legislation waged as hard as was humanly pos- sible. The farmers’ candidates, too, have stuck by their pre-election pledges in a way. which gives great hope for the future. - It shows that there are men too big to be corrupted if the people take the pains to find them. The early League farmers built on faith in a great idea. The farmers who follow will build on what has been accomplished. . dependencies. Today, thanks to the operation of the Gladstonevland act, a larger proportion of the population of Ireland are home-owners than in Scotland, England or Wales. 1 In all these European and Australasian countries the land banks are administered on the same general scheme that is proposed for Nerth Dakota. Administration is by public officers who are responsible directly to the people. There is no intervening corporation_ between -the state and the people. The suc- cessful systems of other countries were fol- lowed in devising the bill for the pro- posed state bank of North Dakota. Advocates of the proposed -state land bank—for that is all the Bank Governor Frazier of North Dakota, in his office at Bismarck, and the presiding officers of the two houses of the North Dakota legislature. On the left is- L. L. Stair,’ speaker of the house of repre- On the right is Lieutenant Governor Howard D. Wood, who presides over the state sen- ate. At the 1917 session of the legislature, Mr. Wood was speaker of the house. All bt three men are actual farmers and hard fighters for the people. v Precedents and Farm Loan Acts—Many Countries Offer Experience of North Dakota really will be—contend that it will accomplish the following results in North Dakota: 1. Put more money in the financial institutions of the state by acting as a reserve for banks that now keep their reserve funds in the Twin Cities. 2. Stabilize financial institutions of the state and add to their security. : 3. Reduce the interest rates and promote in- dustry. : : 4. ‘Put more money in circulation through its guarantee of deposits which will bring out large sums of money now hoarded. . 5. Bring in outside capital by the sale of bonds based on North Dakota real estate. The municipal bank of St. Paul has more than $3,000,000 on de- posit, practically all in small amounts from wage- - earners. It is believed that the Bank of North Dakota will attract depositors of this sort from all the United States and that the bonds will have a ready sale. 6. Promote agriculture as well as develop in- dustry by making money easier to borrow at lower interest. HITS ONLY AT . BANKING EVILS - Every one of the foregoing reasons will benefit bankers as well as business men and farmers. Even the reduction of interest rates, paradoxical as it' may seem, will not injuriously affect bank- ers. It will be an advantage to the real lenders of money. The man who lends money now does not get all of the high rates, the difference being ab- sorbed by other agencies in commissions and pre- miums. Reduction of interest will increase the cer- tainty of payment, add to the value of real estate mortgages and actually operate to the advantage of the local banker who loans his money. The only persons in any way harmed will be the agents who loan outside eapital at commission. Legitimate bankers realize the proposed state institution does not injure their interests and from all parts of the state Nonpartisan league legisla- tors have received letters from country bankers praising the act and announcing their intention of coming in under its terms the moment the law is passed and the Bank of North Dakota organized. Certainly, the proposed land bank will benefit the people of the state as a whole by loaning part of the public funds, part of its deposits, and part of its capital acquired by the sale of real estate bonds, to farmers and others at a low rate of in- terest. . ) REDUCTION IN INTEREST BURDEN At the present time the farm lands of North Dakota are mortgaged for the staggering sum of. $309,000,000. These mortgages for the most part are held by trust companies outside the state and the average rate of interest paid on this gigantic sum is 8.7 per cent. In other’words, the farmers of North Da- kota are paying an annual interest bill of $26,883,000. By loaning money at 6 per cent interest the Bank of North Dakota can enable the farmers to retire these private’ mortgages and replace them by /long-time loans. This will save the farmers of the state. $8,343,000 a year, or nearly $100 for ; each farmer in the state. These are but a few of the benefits made pos- sible by the Bank of North Dakota. They are benefits which have re- sulted wherever land banks have been operated -and this con- “Stitutes the strongest possible reason for be- lieving that here, too, this financial measure will develop home indus- tries, - encourage home building, bring out hidden to locate within the state, increase agricultural pro- duction and promote prosperity in general. state savings, . induce settlers